- Category Finance

- Version37.0.0

- Downloads 1.00M

- Content Rating Everyone

DailyPay On-Demand Pay: A Practical Earned-Wage Access Solution

DailyPay On-Demand Pay positions itself as a payroll-linked service that lets employees access a portion of their earned wages before traditional payday, providing immediate cash flow relief while helping employers improve retention and engagement. Developed by DailyPay, Inc., the product integrates with standard payroll feeds and HR systems, aiming to be a seamless extension of the employer's compensation workflow rather than a standalone consumer wallet. Its core promise is simple: turn hours clocked into flexible funds that users can access on demand, with visibility and controls designed for both workers and administrators. However, the practicality of access still hinges on employer setup, payroll timing, and any per-transfer fees that may apply based on the employer's plan.

What DailyPay Is and Who It Helps

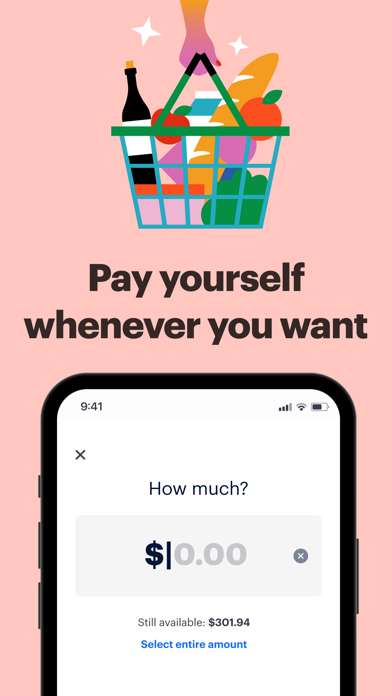

In practice, it's an earned-wage access feature—not a loan or credit line—designed for workers who want to cover urgent expenses or align cash flow with a variable pay cycle. It targets hourly, shift-based, and gig workers who may face irregular income or last-minute bills, offering a predictable mechanism to withdraw wages earned in the current pay period. For employers, it can boost attraction and retention, support scheduling reliability, and demonstrate a tangible commitment to worker financial well-being. The user experience centers on a simple balance view, a transparent available-amount indicator, and a straightforward withdrawal flow that defers to the employer's payroll policy and fund settlement timing.

Core Capabilities: Earned Wage Access and Payroll Synergy

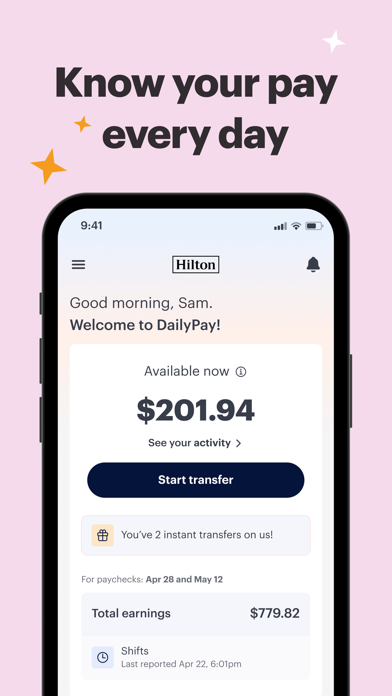

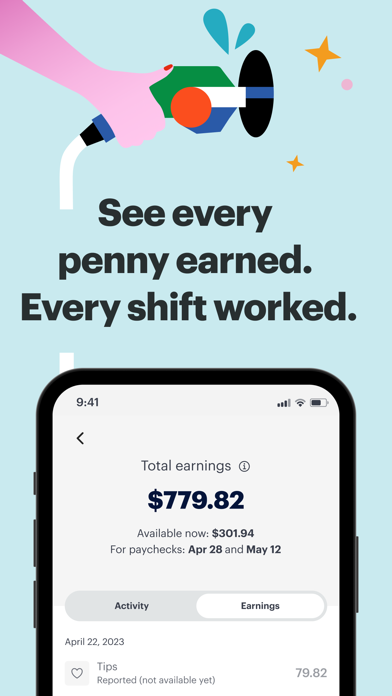

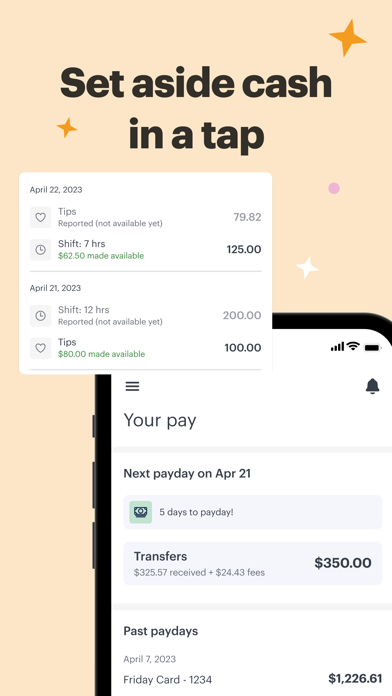

The feature set blends earned-wage access with payroll integration and practical money-management tools. Employees can check an available balance that tracks hours already earned, then initiate transfers to bank accounts or eligible debit cards. Transfers are typically fast—often within minutes—though speed can vary by bank and network; some plans support scheduled withdrawals or batch settlements to align with payroll windows. Employers gain oversight through an admin dashboard that controls eligibility, withdrawal limits, and the timing of fund disbursement, helping ensure the program remains compliant with internal policies and applicable wage laws. Additionally, optional budgeting resources and educational content are sometimes offered to encourage prudent money management. It's worth noting that usage may incur per-transaction fees or be bundled into a broader employer program, so the cost profile should be reviewed in advance.

Earned Wage Access in Practice

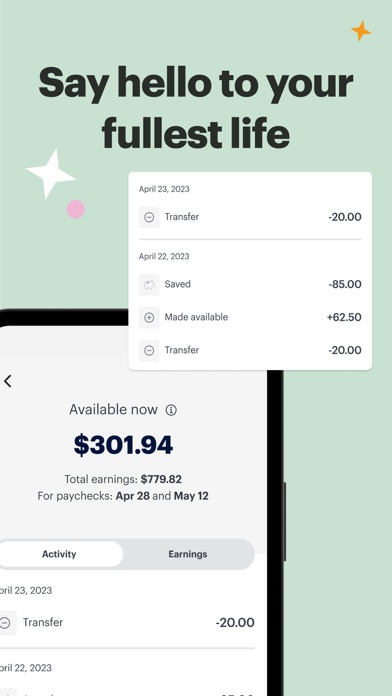

Users see earnings accrued and reflected in real time through a clearly labeled available amount, separate from the upcoming paycheck. When a withdrawal is requested, the app coordinates with payroll feeds to ensure the withdrawal corresponds to wages already earned and to settle the funds against payday. This friction is designed to avoid debt and maintain payroll accuracy; there are usually safeguards such as withdrawal limits per day or per pay period, and reminders when the available amount is exhausted. The result is a fast and controlled mechanism to access earned wages without introducing new debt exposure, with a payment flow that remains traceable in the app and in employer reports.

Design, Onboarding, and User Experience

The app prioritizes a clean, mobile-first design that aims to reduce cognitive load during financially stressful moments. Onboarding is straightforward: users verify identity, link a bank account or card, and connect with their employer's payroll data. The UI emphasizes clarity—clear labels for available funds, upcoming hours, and recent withdrawals—along with concise prompts that guide users through transfers without abrupt interruptions. Response times feel snappy, and the absence of clutter helps users focus on the essential actions: view, withdraw, and review transaction history. For first-time users, a short tutorial and contextual help can reduce any initial uncertainties about eligibility, transfer timing, and fee implications.

Interface and Onboarding: Quick and Clear

From a visual perspective, the interface uses a calm color palette and legible typography that make critical information stand out, such as the available-to-withdraw balance versus the upcoming earnings. The navigation is intuitive, with a central dashboard and a simple action path for requests. Onboarding decisions—like choosing between instant transfers or scheduled settlements—are accompanied by straightforward explanations and opt-in prompts. While the core flow is approachable, there can be nuance in integrating with some employers' payroll feeds, so employers may need to provision test accounts and provide user guidance during the rollout.

Security, Trust, and Competitive Differentiation

Security and compliance underpin DailyPay's trust proposition. The platform uses standard fintech protections—encrypted data transmission, tokenization, and robust authentication options—to safeguard personal and financial information. Access controls, activity logs, and audit trails are available to employers for governance and compliance, while employees benefit from clear receipts of withdrawals and visible history. While specifics may depend on the employer's deployment, the baseline expectation is alignment with common security frameworks and industry best practices for payment processing and data protection. As with any payroll-related service, timing and reliability are contingent on integration quality and the underlying banking network.

Key Differentiators: Security and Transaction Experience

Compared with consumer-only wallets or generic cash-advance apps, DailyPay's differentiators lie in its payroll linkage and the transparency of the withdrawal flow. The earned-wage model ties access to actual labor already performed, which helps manage risk and reduces the likelihood of user debt. The transaction experience—visibility into what's earned, what's available, and when funds will post—appears more predictable for both employees and administrators. For employers, robust admin controls, clear fee structures, and reliable transfer performance help manage cash flow as part of the broader payroll process. While cost structures vary by employer plan, the promise of a tightly governed, payroll-aligned on-demand pay experience remains its core competitive edge.

Pros

Fast on-demand access to earned wages with a simple, low-friction payout flow that lets you withdraw funds before payday.

Fast on-demand access to earned wages with a simple, low-friction payout flow that lets you withdraw funds before payday.

Seamless employer integration that keeps real-time balance and eligibility updated as you work.

Seamless employer integration that keeps real-time balance and eligibility updated as you work.

Transparent upfront fees and budgeting tools help you understand costs and manage finances with confidence.

Transparent upfront fees and budgeting tools help you understand costs and manage finances with confidence.

Mobile-first experience with instant notifications and a clear transaction history for every advance.

Mobile-first experience with instant notifications and a clear transaction history for every advance.

Flexible payout options and tools designed to reduce reliance on high-interest loans.

Flexible payout options and tools designed to reduce reliance on high-interest loans.

Cons

Fees and advance limits can add up when used frequently. (impact: high)

Temporary workaround: limit number of advances per pay period and use budgeting tools; Official improvement: reduce per-advance fees or introduce a cap per cycle.

Not all employers participate in on-demand pay, restricting access for many users. (impact: high)

Temporary workaround: ask HR to enroll or move to participating employer; Official improvement: expand the employer network and add self-service enrollment.

In-app budgeting features could be more granular. (impact: medium)

Temporary workaround: supplement with external budgeting apps; Official improvement: add granular budgeting, goals, and savings.

Over-reliance on advances may disrupt long-term budgeting. (impact: medium)

Temporary workaround: set withdrawal limits and reminders; Official improvement: implement spending prompts and educational tips.

Occasional app glitches or slower support during peak times. (impact: high)

Temporary workaround: contact support via other channels while queue; Official improvement: scale support and improve app reliability.